sur Nanohale AG (isin : DE000A1EWVY8)

Formycon AG Maintains Strong Growth Prospects Amidst Challenging Market Conditions

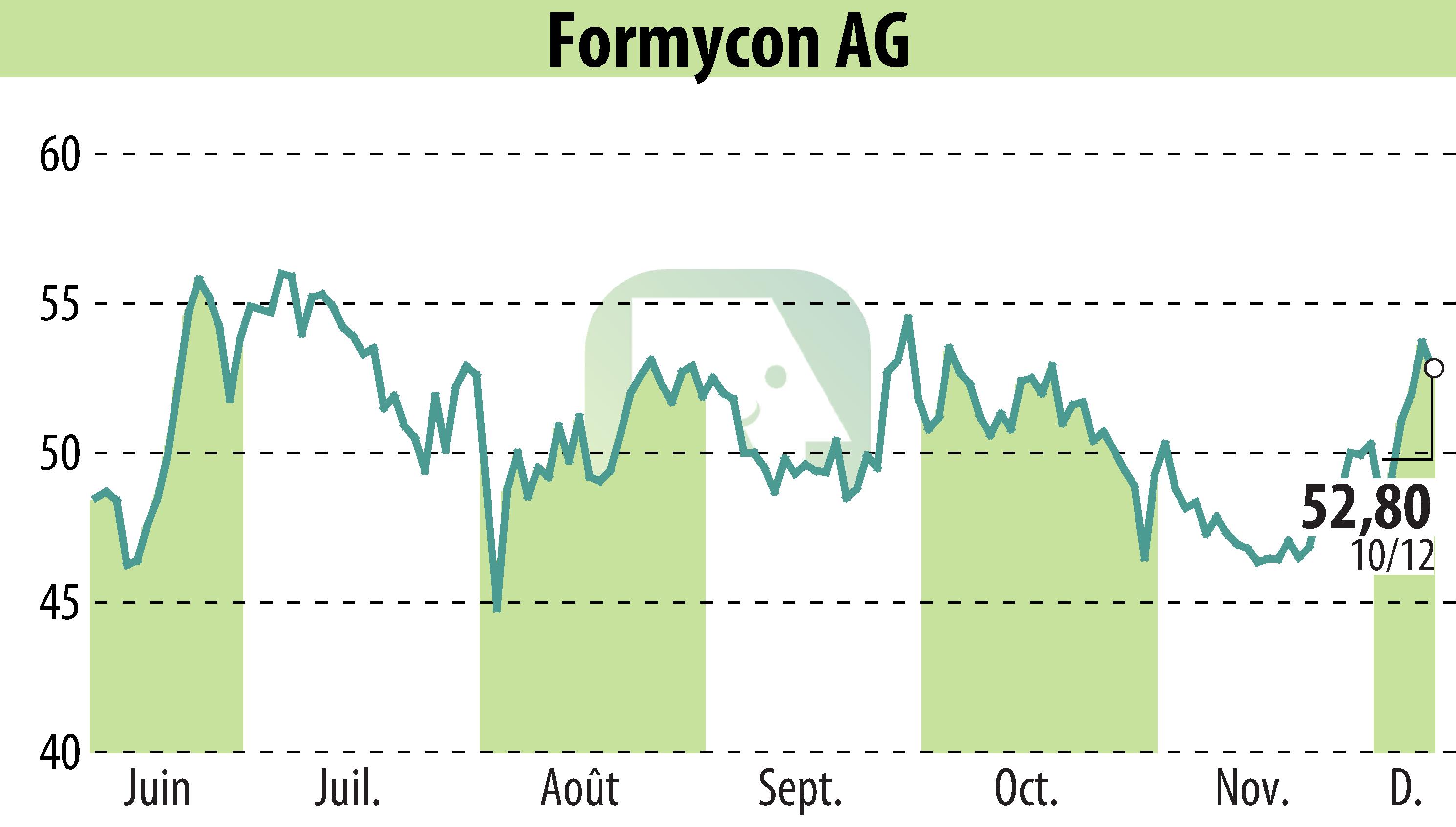

First Berlin Equity Research has reiterated its "Buy" rating for Formycon AG, maintaining a target price of €82. Despite a 31.7% drop in revenue to €41.1 million due to decreased milestone income, the firm remains optimistic about the company's future. The decline was linked to the winding down of development for FYB201 and FYB203 biosimilars.

FYB201, launched in 2022, continues to generate revenue, while FYB203 is expected to launch next year, pending ongoing litigation outcomes. The upcoming launch of the Stelara biosimilar, FYB202, is particularly significant after securing FDA and EMA approvals. Johnson & Johnson's lack of a successor product provides a competitive edge for Formycon.

Royalty income from FYB202 could reach triple-digit million euros by 2026, offering a lucrative opportunity compared to FYB201's expected €15 million royalties. This potential growth supports the current favorable stock valuation.

R. P.

Copyright © 2024 FinanzWire, tous droits de reproduction et de représentation réservés.

Clause de non responsabilité : bien que puisées aux meilleures sources, les informations et analyses diffusées par FinanzWire sont fournies à titre indicatif et ne constituent en aucune manière une incitation à prendre position sur les marchés financiers.

Cliquez ici pour consulter le communiqué de presse ayant servi de base à la rédaction de cette brève

Voir toutes les actualités de Nanohale AG